Current and Future State of US Biosimilars

Alex Brill and Christy Robinson

Fourteen years ago, Congress established a regulatory pathway for biosimilars, direct competitors to branded biologic drugs. To date, the Food and Drug Administration (FDA) has approved 49 biosimilars, referencing a total of 15 originator biologics. Of these, 38 have entered the market, corresponding to 10 reference biologics.

In a new report, Samsung Bioepis notes that, on average, market share for biosimilars reaches 53 percent and biosimilars’ average sales price (ASP) drops by 41 percent over the first three years after market entry. But biosimilar market share and prices vary significantly by therapeutic area. An understanding of these trends not only informs observers about the current state of the US biosimilar market but may offer insights into its future as well.

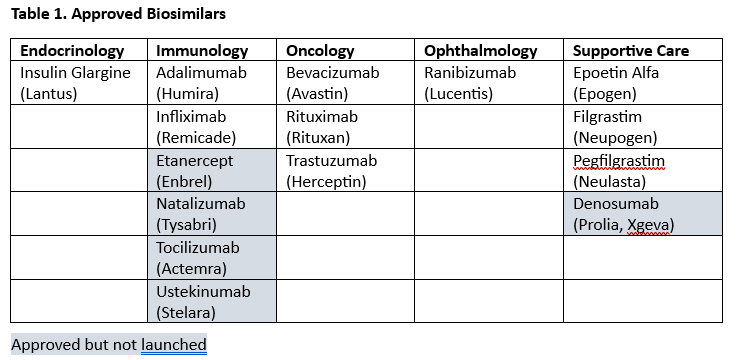

FDA-approved biosimilars fall into five therapeutic areas: endocrinology, immunology, oncology, ophthalmology, and supportive care (for patients being treated for cancer). See Table 1 for molecules with approved biosimilars (reference biologic names in parentheses) in each therapeutic area and whether biosimilars have launched.

Market Share Trends

Oncology represents the greatest success for biosimilars in terms of market share. Oncological biosimilars reached 75 percent market share on average in their first three years on the market and currently have three of the four highest biosimilar market shares by molecule (ranging from 73 percent to 87 percent).

Supportive care biosimilars have had divergent uptake experiences. Filgrastim and pegfilgrastim biosimilars currently have market shares above 70 percent, but epoetin alfa remains below 40 percent. While pegfilgrastim biosimilars were quick to gain a foothold in the market, filgrastim biosimilars had much slower uptake initially.

Ophthalmology and endocrinology each have one molecule subject to biosimilar competition. In ophthalmology, ranibizumab biosimilars launched less than two years ago and have already gained 34 percent of the market. In endocrinology, insulin glargine biosimilars have had very slow uptake, with just 9 percent market share. However, insulin glargine is reimbursed under the pharmacy benefit rather than the medical benefit, making comparisons to other biosimilars difficult, as the pharmacy benefit has different purchasing and prescribing methods.

In immunology, biosimilars for infliximab were initially slow to gain market share but have now captured 48 percent of the market. Finally, the blockbuster immunology biologic Humira (adalimumab) represents the newest biosimilar market, with the first biosimilar launched in January 2023, and the largest in terms of reference product sales. While competition in the adalimumab market was highly anticipated, biosimilar market share was just 2 percent after four quarters—this despite there being six biosimilars competing against Humira by the end of 2023. However, the sluggish start was not entirely unexpected. We wrote last February about why this market would evolve slowly, not least because adalimumab is the first non-insulin biosimilar reimbursed under the pharmacy benefit.

That’s not to say the healthcare market isn’t enjoying savings on adalimumab, as AbbVie has aggressively reduced net prices to maintain market share. In other words, while adalimumab biosimilars have struggled to gain a foothold, their presence has driven Humira to compete to maintain its grasp on the market. However, if the adalimumab market is going to be sustained, biosimilar market share will need to increase significantly. A good sign in this direction is the sudden sevenfold increase this month in biosimilar adalimumab market share (from 5 percent to 36 percent). This jump is largely attributable to one of the major pharmacy benefit managers (PBMs), CVS Caremark, replacing Humira on its formularies with an adalimumab biosimilar marketed by a CVS company in partnership with Sandoz.

Price Trends

As with market share, biosimilar pricing trends vary by therapeutic area. According to the Samsung Bioepis report, oncological biosimilar price discounts are relatively steep—bevacizumab, rituximab, and trastuzumab biosimilar ASPs are, on average, 49 percent, 70 percent, and 76 percent below the pre-biosimilar reference product ASP, respectively—while oncological reference products maintain high ASPs. It is worth noting that pre-biosimilar ASPs of reference biologics in this therapeutic area were significantly higher than they were in all other biologic markets besides one (pegfilgrastim/Neulasta).

In supportive care, reference product Neupogen maintains a high ASP while biosimilar filgrastim manufacturers have brought the average biosimilar price to 67 percent below the pre-biosimilar Neupogen price. In the other two supportive care biosimilar markets (epoetin alfa and pegfilgrastim), the reference biologic competes on price with biosimilars, and biosimilar price discounts average 41 percent and 56 percent, respectively.

Remicade has also cut its price to compete with infliximab biosimilars in immunology. On average, infliximab biosimilars are 73 percent lower than the pre-biosimilar Remicade price. Lucentis, the ophthalmology biologic newly subject to biosimilar competition, immediately dropped its price when a biosimilar entered the market. Currently, the biosimilar discount in the ranibizumab market is only 18 percent, but as time passes and more biosimilars enter the market to compete with Lucentis, the prices will likely fall further.

As noted above, the markets for insulin glargine and adalimumab are different than other biosimilars because they are reimbursed in the pharmacy benefit of insurance plans rather than the medical benefit. Since only medical benefit products have ASPs, Samsung Bioepis provides wholesale acquisition cost (WAC) data for insulin glargine and adalimumab. Some insulin glargine and adalimumab manufacturers employ a two-price strategy, with one high WAC price and one low. As we wrote last April, the higher WAC leaves room for PBMs to negotiate volume rebates on behalf of health insurance plans and large employers.

While the low WAC price for these biosimilars is a substantial discount off the reference biologic price, it is difficult to know the net price of biosimilars with higher WAC prices because rebate negotiations with PBMs are confidential. Therefore, it may take longer and be more difficult to estimate the savings achieved by adalimumab biosimilars even as they gain market share.

While competition has clearly led to significant price declines for key products over time, there is also a meaningful price floor for biosimilars that distinguishes this market from small-molecule generics. High development and manufacturing costs for biologic drugs limit a competitive biosimilar market from realizing the degree of price competition commonly observed among traditional generics.

Conclusion

The biosimilar market will surely continue to expand in the next few years as more blockbuster biologics come off patent. However, the Inflation Reduction Act of 2022 (IRA), which included a provision to allow the federal government to negotiate a select number of drug prices in Medicare, has some stakeholders concerned that biosimilars will become obsolete. Compounding the IRA’s implications for biosimilars are two additional challenges highlighted by the biosimilar market data presented above.

First, while the recent gain in market share for one adalimumab biosimilar is encouraging, the market is still in its early stages. The fate of other adalimumab biosimilars—and other pharmacy-benefit biosimilars in the future—as well as the decisions of other PBMs remain unknown. Hopefully, we will continue to see progress toward a broader, competitive market.

Second, while the ability of medical-benefit biosimilars to gain significant market share and drive sizeable savings across multiple markets and therapeutic areas is impressive, it is important to remember that the reference biologics with biosimilar competition have large markets. The larger the market, the more competitors are likely to enter. But for non-blockbuster biologics, the degree of competition that can be expected is less clear. The ability to realize savings in smaller biologic markets will depend on whether manufacturers anticipate a large enough return on investment to develop a biosimilar. For this reason, it is a good sign that the FDA has been discussing streamlining biosimilar development and recently proposed a legislative reform to permit all biosimilars to be interchangeable.