Mar 20, 2018 | Analysis

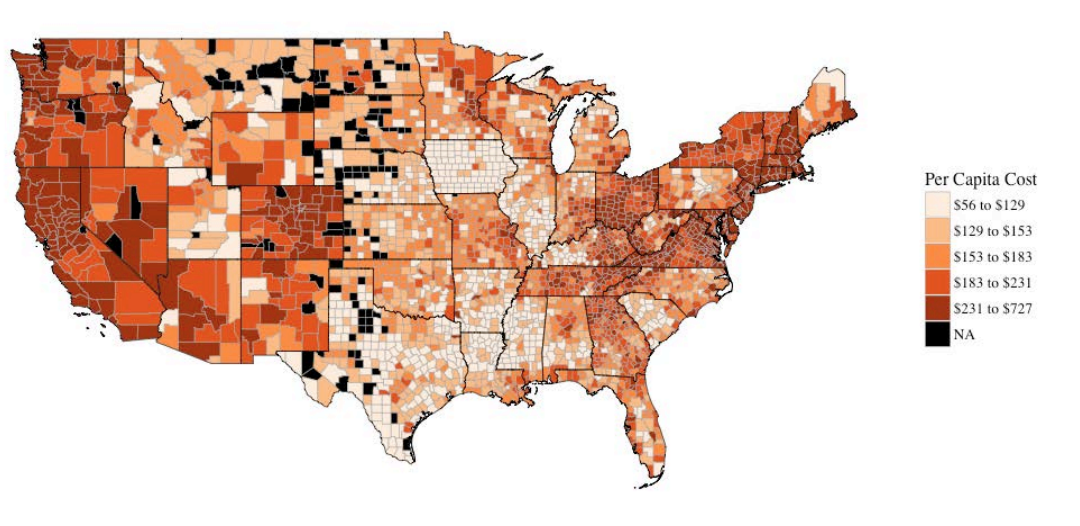

As the opioid epidemic worsens in the United States, the toll it imposes on the US economy has risen to staggering heights. The White House Council of Economic Advisers recently estimated the economic burden, inclusive of the value of statistical lives lost, to be $504 billion in 2015. More narrowly constructed estimates find cost burdens as high as $95 billion in 2016.

Mar 12, 2018 | Interviews

While discussing the recent job report and unemployment rate, Alex Brill said “it’s a phenomenal number in terms in job creation. Unemployment rate another phenomenal number. Our unemployment rate is basically stuck at 4.1. Last time it was five months in a row was back to 2012 when it was double the rate it is today. So we are seeing an economy near full employment with numbers that are really surprising this late in the cycle.”

Mar 9, 2018 | Events

Alex Brill joined the Tax Foundation for a panel discussion on what the federal tax policy debate will look like over the next decade. He shared, “the idea that tax reform will need more work, saying that a sound policy must be sustainable and predictable. And he argued that Congress should consider new ways to broaden the tax base to afford more sound, pro-growth reforms.”

Mar 6, 2018 | Testimony

The passage of time and changing circumstances have rendered the physical-presence requirement articulated in National Bellas Hess, Inc. v. Department of Revenue, 386 U.S. 753, 758 (1967), and Quill Corporation v. North Dakota, 504 U.S. 298, 324-15 (1992), a harmful anachronism. Standard tools of economic analysis that the Court considered in Comptroller of the Treasury v. Wynne reveal that South Dakota’s sales and use tax regime, as amended by S.B. 106, promotes neutral treatment of in-state and interstate commerce. By contrast, the bright-line physical-presence requirement set forth in Bellas Hess and Quill forces states to extend what is in practice a discriminatory subsidy in favor of a specific class of out-of-state sellers, namely, those sellers who lack a physical presence within the state. On the facts of the challenged statute, there is no valid economic reason to mandate such a discriminatory subsidy.

Mar 5, 2018 | News

“[Alex] Brill noted that other developed countries have already begun to reduce, or have proposed reducing, their corporate rates in response to the Tax Cuts and Jobs Act (P.L. 115-97), which has in turn prompted some concerns of a “race to the bottom” of countries competing with each other by shrinking their corporate tax revenue base. If the United States reverted to a 35 percent corporate rate or even just partially undid the rate cut, it could put itself at an even greater competitive disadvantage than it was in before the TCJA’s passage, Brill said.”