Jun 18, 2018 | Analysis

This paper investigates how the Tax Cuts and Jobs Act affects household charitable giving in the United States. We find that the law will reduce charitable giving by $17.2 billion (4.0 percent) in 2018 according to a static model and $16.3 billion assuming a modest boost to growth.

Mar 20, 2018 | Analysis

As the opioid epidemic worsens in the United States, the toll it imposes on the US economy has risen to staggering heights. The White House Council of Economic Advisers recently estimated the economic burden, inclusive of the value of statistical lives lost, to be $504 billion in 2015. More narrowly constructed estimates find cost burdens as high as $95 billion in 2016.

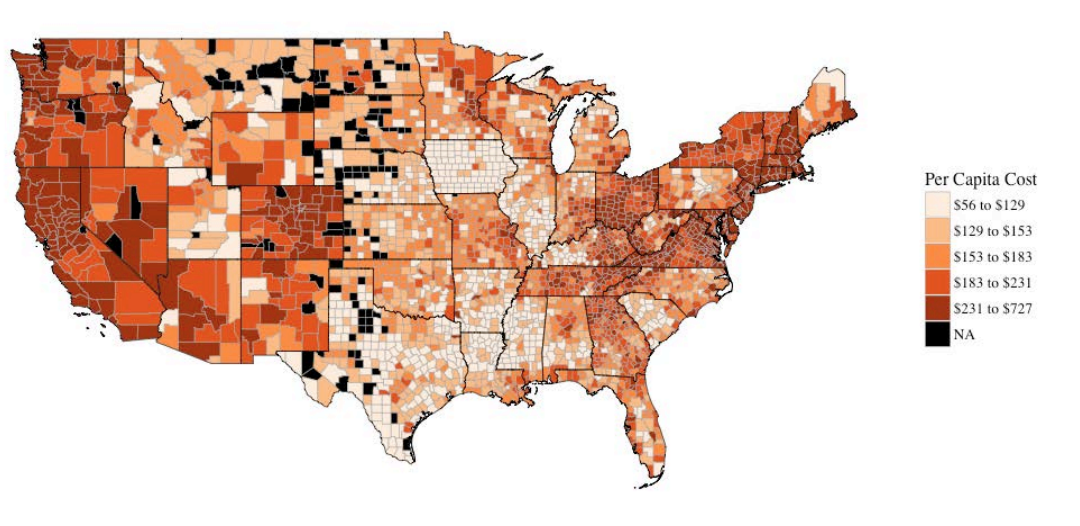

Feb 1, 2018 | Analysis

This report investigates the impact of a revenue-neutral carbon tax whereby revenues raised from a $25/ton carbon tax are used to reduce the tax rate on wage income by a commensurate amount. Recognizing that such a reform is not revenue-neutral for every single taxpayer, nor even revenue-neutral in every county, we investigate the degree of spatial variation across all counties and sort results by the historical partisan preferences of those counties.

Nov 30, 2017 | Analysis

The United States is slowly but surely headed toward a federal debt crisis certain to inflict serious economic hardship on future generations. Today, the amount of federal debt held by the public stands at $14.8 trillion (all figures in this paper are in US dollars). While the US economy is expected to grow 76 percent in the next 30 years, that debt burden will, in inflation-adjusted terms, increase by over 240 percent during that time. Returning to a sustainable fiscal outlook will require hard choices and a clear understanding of both what led us to this point and the economic consequences of inaction.

Nov 29, 2017 | Analysis

Federal fiscal reform in the United States is increasingly necessary but over the last two decades has remained elusive. Part of the reason for the inaction reflects different political preferences and priorities. Part of it reflects differing views about the possible economic and social effects of controlling public spending and fiscal deficits. The result is that the US federal debt continues to grow unabated, which poses an increasing threat to future generations of citizens.

Oct 16, 2017 | Analysis

“As the result of this infuriating tactic, patients, insurance companies and the federal government pay an additional $5.4 billion annually on drugs, according to a study by Matrix Global Advisors for the Generic Pharmaceutical Association.”